Roughly five hundred well-established U.S. companies comprise the S&P 500. Each one is held under a microscope every second of every day. Probing eyes scrutinize and analyze each tick of the stock market and assess value according to price. But unfortunately, such intense magnification can prevent us from seeing the bigger picture.

There Is a Market for Companies, And There Is a Market for Stocks. But Are They the Same?

The truth is that there’s an incessant disconnect between each relationship. Technically, the two are of a piece, but serious investors would be well-served to focus more on the value of the companies rather than the price of the stocks comprising them.

The value of a company is typically enduring and glacial. But, on the other hand, its stock price is often as frantic as a yappy dog with a Napoleon complex. The latter is used as content fodder for the never-ending daily news cycle, triggering the release of the cortisol and adrenaline hormones that provoke anxiety and hyperbolic despair. This emotional spark, by the way, is one reason media outlets churn out stock news so early and often. Leading the primetime hour with a story about the stability of company values may be a path to happiness in retirement, but it doesn’t necessarily lead to higher TV ratings.

Making this critical mental shift from stocks to companies can be particularly helpful, especially in a year as tough as the one we’ve experienced. We’ve witnessed an out-of-balance Consumer Price Index (CPI), wage inflation, commodity inflation, housing inflation, gas inflation, and angsty predictions about what the Fed will do to combat rising prices.

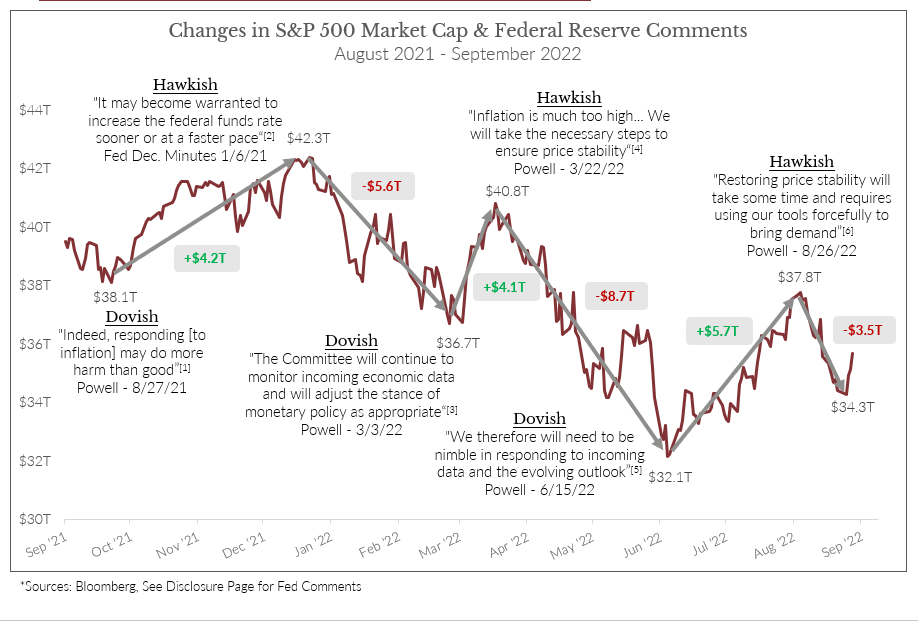

My team recently created a chart that shows the S&P 500 overlayed with big Fed announcements dating back to last August, and the visual is crystal clear. In general, when the Fed was dovish, stock prices rallied, and when it was hawkish, stock prices fell. As a reminder, a dovish Fed policy favors lower interest rates as compared to a hawkish Fed that prefers higher interest rates.

This data reveals the fluctuation of trillions of dollars merely because of a few comments from the Fed. For example, the S&P 500 sat at $21 trillion in the depths of the pandemic. However, in January of 2021, it was up to $40 trillion.

What does this tell us? First, the Fed is highly influential. Second, it demonstrates that the frenetic action of stock prices is primarily based on the mood investors are in that day. In other words, companies don’t quickly gain or lose trillions in value, but stock prices act as if they do. Shelving the microscope and zooming out to look at the market as companies, rather than stocks, provides so much perspective.

What Do We Know About Publicly Traded U.S. Companies?

They are a collection of people, intellectual property, and brand value. They have bountiful financing, talented managers, continual innovation, and typically thousands of dedicated humans with a natural incentive to move the mission forward. You know these companies. You depend on these companies for your goods and services.

Think about where you buy groceries, how you ship packages, and how you transport yourself to work or vacation. Ponder how we light our homes, how we heal our sick loved ones, and how we protect our nation from threats, both foreign and domestic. Public companies in the U.S. are part of the very fabric of American life. We’re not a perfect nation, but our brand of capitalism operates like a mighty army of American productivity.

The good news is that we can invest in these highly dependable businesses for the duration of our lives, into retirement and beyond. The bad news is that we do that in the form of investing stocks.

Wait a minute, doesn’t that mean we’re back to square one? Aren’t stocks just a hyper and emotional reflection of how short-term traders feel about companies minute by minute? Yes. But stay with me here. Even though companies and stocks are the same, they’re also not.

Companies try to grow their earnings little by little each year. They get to set the prices paid, even in inflation. As long as those earnings grow over time, the company can increase its overall size and its dividends to shareholders. To put it another way, companies allow you to invest in marathons compared to the tumultuous sprint of the stock game.

Stock Prices Should Generally and Eventually Reflect the Earnings of Companies

The important exception is one that helps me make my case—over the long run, stock prices should generally and eventually reflect the earnings of those companies. This result won’t necessarily happen in any given year but throughout ten, twenty, thirty, and forty years.

Here’s what I mean.

Company earnings for the S&P 500 sat at roughly $5.50 back in 1970. The S&P 500 sat around 100. Let’s fast forward to today. Projected earnings for the S&P 500 for 2022 are around $225, with the S&P 500 at about 4000. Both of those increases are forty-fold over that time!

The problem is that you’re not Rip Van Winkle in the real world. You’re wide awake and seeing the chaotic shifts in stock prices. Twenty minutes feels like twenty years, not the other way around. I always tell my clients to avoid obsessively checking prices, but it’s tough. Stock reports are everywhere, and those gnarly crashes are scary. But, because of that army of productivity, they bounce back over time. The key is to look away from the daily swings in stock prices and trust that the market should correct itself.

Put yourself in a position to be constantly reminded that you are investing in companies, not stocks. Have a long-term plan for retirement and trust it. Remind yourself of the enduring power of companies, earnings, and dividends. Save yourself from the perils of price and enjoy the confidence of companies. For many, this is one of the deciding factors of a happy vs. unhappy retirement.

This information is provided to you as a resource for informational purposes only and is not to be viewed as investment advice or recommendations. Investing involves risk, including the possible loss of principal. There is no guarantee offered that investment return, yield, or performance will be achieved. There will be periods of performance fluctuations, including periods of negative returns and periods where dividends will not be paid. Past performance is not indicative of future results when considering any investment vehicle. This information is being presented without consideration of the investment objectives, risk tolerance, or financial circumstances of any specific investor and might not be suitable for all investors. There are many aspects and criteria that must be examined and considered before investing. Investment decisions should not be made solely based on information contained in this article. This information is not intended to, and should not, form a primary basis for any investment decision that you may make. Always consult your own legal, tax, or investment advisor before making any investment/tax/estate/financial planning considerations or decisions. The information contained in the article is strictly an opinion and it is not known whether the strategies will be successful. The views and opinions expressed are for educational purposes only as of the date of production/writing and may change without notice at any time based on numerous factors, such as market or other conditions.

Fed Comments:

[1] https://www.federalreserve.gov/newsevents/speech/powell20210827a.htm

[2] https://www.federalreserve.gov/monetarypolicy/files/fomcminutes20211215.pdf

[3] https://www.federalreserve.gov/newsevents/testimony/powell20220302a.htm

[4] https://www.federalreserve.gov/newsevents/speech/powell20220321a.htm

[5] https://www.federalreserve.gov/mediacenter/files/FOMCpresconf20220615.pdf

[6] https://www.federalreserve.gov/newsevents/speech/powell20220826a.htm