If stock dividends had their own headline, this might be it: Dividend income ignored due to pricing in cents.

Let me start with a quick story from home that inspired this topic.

One recent weekend, I was walking my German shepherd and 90-pound Lab — or rather, they were walking me. It was a spectacle of sorts as you can imagine with two dogs who had been cooped up after several days of rain. Joining me on the stroll down Peachtree Street was Jake, my third grader.

Despite the chaos caused by the two animals, Jake spotted something shiny on the sidewalk. It turned out to be a Sacagawea dollar coin.

This was the discovery of the century for Jake, who couldn’t hide his excitement. “Dad, this is like a treasure!” he said.

Lying next to the dollar coin was an old penny, which he left lying on the ground.

“Jake, what about the penny?” I asked him.

“Dad, a penny doesn’t even buy a piece of candy these days,” he said.

Jake’s treasure discovery showed me the lack of enthusiasm for anything denominated in cents anymore. It’s the almighty dollar that rules. In the case of stock dividends, however, pennies can add up to a tsunami of cash flow. Let me explain.

How dividends work

Dividends are a way for a company to give back some of its profits to shareholders. They’re cash payments that some companies give to investors. Dividend amounts are seemingly small as they are often paid out and announced in small increments per share. For example, it’s not uncommon for a company to pay 50 cents or 60 cents per share as their dividend, divided into four quarterly payments. Like my son, Jake, the public rarely gets excited about this concept. As on the surface, dividends might not seem to add up to all that much.

Perhaps an even more ignored creature is the dividend increase, which is typically only a few cents in any given year. For example, if you own stock in a company that pays a dividend of 57 cents per share, they may announce a dividend increase of 4 cents to 61 cents. That means you get an extra 4 cents for each share you own.

What’s the big deal? It’s only 4 cents.

Well, 4 cents on 57 cents is a 7% dividend increase on each share you own. If the dividend went up by this amount every year, it would double in about 10 years. Yes, double. Over time, if you stick with dividends, the money will begin to pour in.

I think the reason dividends don’t get the recognition they deserve has a lot to do with their payout in the smallest of economic increments — cents. However in 2019, S&P 500 companies alone paid out $485 billion in dividends to shareholders. Starting to look like more than a few cents, right?

The study: Dividend income vs. bond interest

Now, let’s have a look at the income-producing power of stock dividends vs. bond interest using the S&P 500 vs. the Aggregate Bond Index. As a reminder, bonds are essentially IOUs issued by governments or companies. Investors buy these loans, and the issuer promises to pay them back in full plus interest along the way.

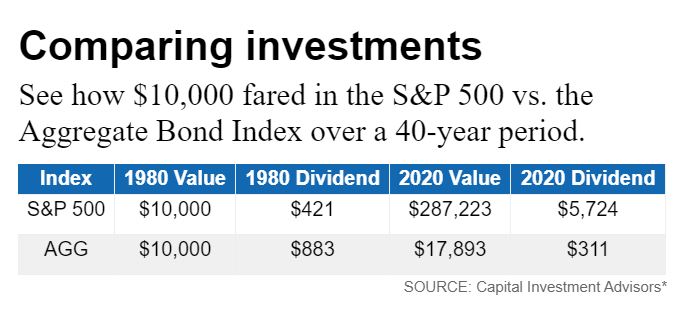

My team at Capital Investment Advisors put together a 40-year study that compared a $10,000 investment in the S&P 500 vs. the Aggregate Bond Index. In each case, investors left the principal alone while taking the income produced each year by the dividends.

The table below shows what happened over time with each investment.

Back in 1980, a $10,000 investment in the S&P 500 paid a dividend of about $421, or 4.21% on the initial investment. Forty years later, the dividend income had climbed to $5,724. That’s a 57% annual yield on the original investment.

Over the next 40 years, the income from stock dividends grew at about 6% per year. During that same period, inflation grew at about 3%. Which means dividends doubled the rate of inflation. Talk about protecting your purchasing power.

Don’t forget that the original investment grew as well. If you had invested $10,000 in the S&P 500 in 1980, your investment would have grown into more than $287,000 as the stock price increased. That’s not counting the dividend income you received each year.

This price-only return (which excludes dividend income) clocks in at about 8.75% per year. If you add in another 3% for the dividends you receive each year, you get a total return of about 11.75% per year.

On the other hand, the Aggregate Bond Index grew from $10,000 to only $17,893 and would now pay you only $311 per year, or 1.75% on your investment.

As you can see, income from stock dividend easily outpaced bond interest. Annual stock dividend income increased over 13.5 times in price, while the remaining price-only return grew 28 times. Bonds, on the other hand, rose less than two times in price, with a 64% reduction in income.

It doesn’t matter if you have $500,000 or $5 million in your retirement portfolio. It’s hard to find a more consistent source of growing income to outpace inflation than dividend-paying stocks.

The verdict: Dividends are a powerful wealth-building source that should not be ignored

You might be saying to yourself, “That would have been nice over the last 40 years, but haven’t I missed the boat?” Not really. If you’re 40 or 50 years old, you still have three to four decades left to invest, even into your retirement. You have more years of spending ahead of you than you might think. Think in decades, not years.

Look for stocks that are perennial dividend payers and consistent dividend growers. Then be patient, and watch the dividends come in over time. Remember: Despite prices going up and down, dividends from established American companies have a tendency to remain relatively steady. Even in tumultuous years like 2020.

Be patient. You’ll find that those pennies start adding up over the years. And you’ll be happy you picked them up. This pursuit of dividends is perhaps worthy of a life’s work for any investor with the long-term patience and vision to do so.

*The Capital Investment Advisors research department completed this study, and a link to more information and this in chart form can be found on wesmoss.com.

Wes Moss has been the host of “Money Matters” on News 95.5 and AM 750 WSB in Atlanta for more than 10 years now, and he does a live show from 9-11 a.m. Sundays. He is the chief investment strategist for Atlanta-based Capital Investment Advisors. For more information, go to wesmoss.com.

Read the original AJC article here.

Disclosure: This information is provided to you as a resource for informational purposes only. It is being presented without consideration of the investment objectives, risk tolerance or financial circumstances of any specific investor and might not be suitable for all investors. Past performance is not indicative of future results. Investing involves risk including the possible loss of principal. This information is not intended to, and should not, form a primary basis for any investment decision that you may make. The information contained in this piece is not considered investment advice or recommendation or an endorsement of any particular security. Further, the mention of any specific security is solely provided as an example for informational purposes only and should not be construed as a recommendation to buy or sell. Always consult your own legal, tax or investment advisor before making any investment/tax/estate/financial planning considerations or decisions.