When retirement time rolls around, some folks find themselves pondering a change of address. So I run into this question a lot – to rent or to buy? Whether you’re contemplating relocation to a new city or just downsizing for convenience, it’s worth considering both options.

As always, the answer will depend on your unique circumstances and goals. Even if you haven’t been a renter since the days of wood paneling and wall-to-wall shag carpets, you may find yourself considering the option in retirement. Some retirees welcome the freedom renting affords – it’s easier to pull up stakes and move somewhere new if a steady change of scenery is your thing. Others prefer the rootedness and security that comes with being a homeowner.

No matter your personal lifestyle preferences, remember that housing is a huge expense. So before you make your next move, it’s a good idea to run the numbers. There are a plethora of online calculators that can help you tally the costs over time of renting versus buying.

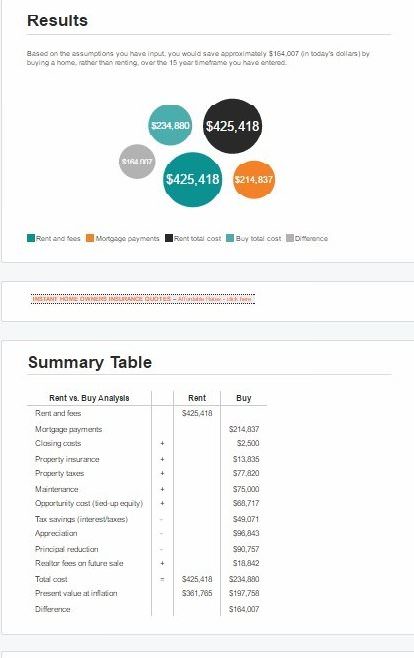

Take this hypothetical, for example. I used the online calculator at Calcxml.com to generate real numbers that would tell the financial story of renting compared to buying a home. For the calculations, I used a home valued at $280,000. The rental price was estimated at approximately $2,000 per month, and I included costs for rental insurance ($50 per month) and annual rent increases (of 2% per year). I assumed a tax bracket of 25%.

Side-by-side, I compared purchasing the same house. With a purchase price of $280,000, I included the following incidental costs: amount of the mortgage loan ($250,000); annual interest rate (4%); number of years financed (30); closing costs ($2,500); annual homeowner’s insurance premium ($800); annual property taxes ($4,500); yearly maintenance allowance ($5,000); annual appreciation rate (2%); and realtor fees on future sale (5%).

After inserting all these variables, I let the calculator do the rest. The result? Over a fifteen-year time period, buying this house would result in a cash positive benefit of almost $165,000 over the alternative of renting.

While this calculation provides a useful comparison, it is by no means definitive. Money aside, there are benefits to both renting and buying. What the calculators can’t capture are personal preferences – things like the importance of convenience and mobility, whether you want to leave a home as an inheritance, and how long you want to be in your new home.

So check in with yourself on important lifestyle questions. Maybe you love the idea of owning a new place and fixing it up exactly the way you want. Or perhaps you breathe a big sigh of relief after years of home ownership when you imagine not worrying about lawn maintenance or a broken sump pump.

As a final note: keep in mind too that your first move during retirement may not be your last. Given how long retirement can last these days, you could find yourself changing addresses several times, and switching between renting and buying, along the way. Who knows? You may even see a renaissance of shag carpeting. Although, somehow I doubt it.

Read the original article here.

Disclosure: This information is provided to you as a resource for informational purposes only. It is being presented without consideration of the investment objectives, risk tolerance or financial circumstances of any specific investor and might not be suitable for all investors. Past performance is not indicative of future results. Investing involves risk including the possible loss of principal. This information is not intended to, and should not, form a primary basis for any investment decision that you may make. Always consult your own legal, tax or investment advisor before making any investment/tax/estate/financial planning considerations or decisions.