Securing retirement happiness often requires fighting against financial tunnel vision. Having enough in the bank is the starting point, not the finish line. That said, you can’t win the race without starting it. Money doesn’t generate automatic happiness, but living your best life without it often proves challenging. Learning the Five Money Secrets Of The Happiest Retirees can be enormously helpful.

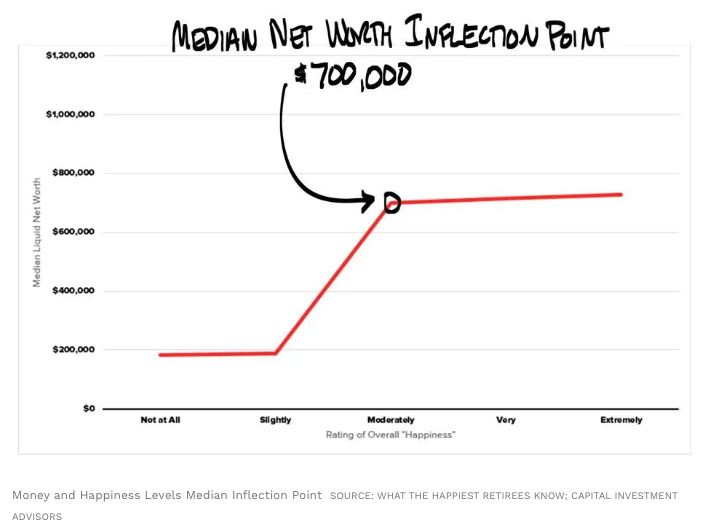

Habit #1: The Happiest Retirees Have A Minimum Of $700,000 In Liquid Retirement Savings

Based upon a nationwide survey of roughly 1,350 retirees researched in writing You Can Retire Sooner Than You Think and What the Happiest Retirees Know, the research (adjusted for inflation) found that the happiest retirees have a minimum of $700,000 in liquid retirement savings, with a few caveats. First, liquid retirement savings must be easily accessible: stocks, bonds, mutual funds, and cash. You don’t need a Scrooge McDuck-styled room of gold coins, but an obscure Pablo Picasso bird-shaped ceramic vase that can’t be sold without 10 years of legal certification doesn’t count.

It should also be noted that $700,000 is a “median” calculation, meaning the number that falls in the middle of the list. Looking at the “average” amount, the happiest retirees have $1.25 million (mean) in liquid retirement savings. But the median can often be more illuminating as a data point and is emphasized here.

When You Can Retire Sooner Than You Think was published in 2014, $500,000 in liquid savings was the critical inflection point for a happy retirement. The world has changed, with massive inflation being the most glaring development. From 2013 to 2020, inflation was a manageable 12%. Then came the COVID pandemic and its subsequent adjustments and consequences, leading inflation to nearly 20% from 2020 to 2023. These new figures incorporate inflation plus a safety buffer: a total of 40%.

Of course, there are happy retirees with less than $700,000, but the research shows significant improvements in happiness levels from $0 to $700,000. Having more is fine, but happiness tends to level off after $700,000 due to the Plateau Effect.

Individual economic needs vary. Some claim $700,000 is exceptionally high, while others find it too low. If that sounds insurmountable, don’t panic. It requires considerable time and hard work to accumulate that kind of wealth, but it is by no means impossible.

Habit #2: Get The Mortgage Paid Or Have Payoff Within Sight

According to research from my 2021 book, What The Happiest Retirees Know, retirees within five years of mortgage payoff are four times more likely to be happy. As the years to pay off the mortgage tick down, happiness levels go up. This revelation was surprising, but surveying over 1,350 families left little doubt.

Mortgage payments are typically the most significant, scariest expenditures. A home loan represents the basic human need for shelter, without which residents are thrown to the wolves. In my neighborhood, it’s more like being thrown to the golden retrievers, but you get the point.

Despite its gravity, the mortgage can be a discouraging, repetitive payment. The weighty output is not for travel, school, or enjoyment but rather a giant subtraction without any immediate satisfaction. Conversely, having no mortgage responsibility is a massive relief on so many levels. Your home is yours, free and clear, and that hefty monthly debit can go toward fun, family, and living life to the fullest.

The counterargument often insists you can make more money holding on to the mortgage and investing your savings. It relies on the premise that the interest paid on the mortgage will equal less than the interest and returns earned in the market—a point of view worth discussing when mortgage rates were sub-3% but more dubious at the current rate of nearly 7%.

How should you decide? The One-Third Rule is typically a valuable rule of thumb. If you can pay off the mortgage using no more than one-third of your non-retirement savings, consider doing so. For example, if you have $150,000 in non-retirement savings and only owe $40,000 on the mortgage, you might consider paying it off.

I’ve learned from the happiest retirees that serenity comes from owning your home outright. It also dramatically lowers monthly retirement living expenses, taking pressure off the nest egg and other monthly income sources. For these reasons, the pros of paying off the mortgage seem to outweigh the cons.

Habit #3: Have Multiple Streams Of Income

From my research, happy retirees average approximately three separate income streams, while the unhappy group averages less than two.

Imagine you were going to receive $10,000 per month for the rest of your life. Would you want one $10,000 check in the mailbox or ten different $1,000 checks? You would want ten checks so that not all your eggs were in one basket. Heaven forbid that basket broke; you’d be in big trouble.

Multiple income streams can flow from various sources: Social Security, rental property, pensions, income from an IRA/401k/brokerage account, etc. These multiple streams can also allow for more flexible tax planning strategies. Lastly, income diversification can be psychologically advantageous because it offers increased control.

Habit #4: Be A Tomorrow Investor

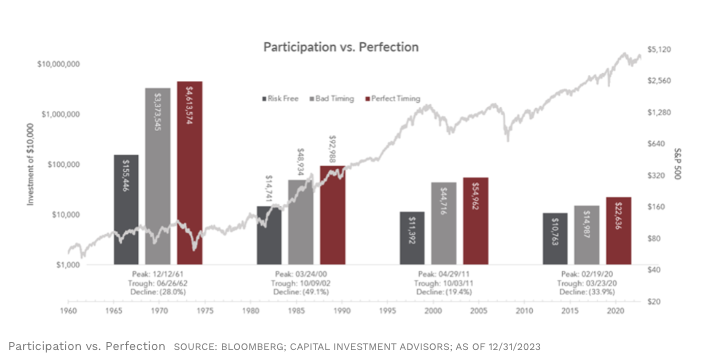

Happy Retirees understand that investing is more about participation than perfection. If you wait until the perfect time to invest, you’ll never do it. Even bad market timing is generally better than being completely out of the market. As investors, that can feel counterintuitive, but the numbers tell a clear story.

The data points above illustrate how a $10,000 investment in the S&P 500 can grow over a particular period. Each relevant year fell on the precipice of a stock market correction.

The data tally results as of December 31, 2023, if you had chosen to invest the $10,000 during each of the following situations:

- Perfect Market Timing—when the market was at the bottom of the cycle.

- Worst Market Timing—right at the market’s peak.

- Holding Money In Treasury Bills —essentially equates to sitting in cash.

Here’s how the numbers compare for selected periods of 60-plus years, 20 years, 10 years, and three years.

Long, Long Run—60 Years—Initial Investment In The Early 1960s

This example reiterates that long-term investing can be effective. Looking at 1961, let’s see what $10,000 invested at the absolute bottom of the 1960s bear market is worth (perfect timing) vs. investing at the 1961 peak (worst possible timing) vs. leaving the $10,000 in T-Bills to avoid all risk.

- Perfect Timing: $10,000 became $4.6 million.

- Worst Timing: $10,000 became $3.4 million.

- T-Bills: $10,000 grew to about $155,000.

Long-ish Run—Roughly 20 Years—Initial Investment From 2000-2002

The worst possible time was the market peak in March of 2000 vs. the best possible time at the market trough in October 2002.

- Perfect Timing: $10,000 became $93,000.

- Worst Timing: $10,000 became $49,000.

- T-Bills: $10,000 is now just under $15,000.

Even the worst stock market timing would have netted you over three times what T-Bills generated.

Intermediate Run—Roughly 10 Years—Initial Investment In 2011

2011 was another year with a bear market decline (-19.4%). Both the peak and trough hit in 2011.

- Perfect Timing: $10,000 became $55,000.

- Worst Timing: $10,000 became $45,000.

- T-Bills: $10,000 would be worth about $11,400.

Short Run—Roughly Three Years—2020 Pandemic Crash

Imagine you were about to invest $10,000 before the pandemic hit but waited and managed to bullseye the March 2020 bottom.

- Perfect Timing: $10,000 became roughly $22,600.

- Worst Timing: $10,000 became almost $15,000.

- T-Bills: $10,000 didn’t even reach $11,000.

Because interest rates were so low, T-Bills barely moved, whereas investing at the worst possible moment still earned you nearly $5,000.

The happiest retirees are tomorrow investors. They understand market history, which helps them focus on participation, not perfection. In every scenario outlined above, investing at the “worst” time bested holding cash. The same culprit is almost always responsible for bailing on the market: fear and uncertainty. Happy retirees rise above those impulses.

Habit #5: Spend Wisely Using The 4 Percent Plus Rule of Thumb

In 1994, William Bengen, a Massachusetts Institution of Technology aeronautics and astronautics graduate turned financial planner, calculated stock returns and retirement scenarios for the previous 75 years. He found that retirees who drew down 4% of their portfolio in the first year of retirement, adjusting every year for inflation, would likely see their money outlive them, assuming the portfolio had a 50-75% allocation to stocks.

Based on his calculations, nest eggs last 50 years 80% of the time. In the worst-case scenario, the money still lasted 35 years. The 4 Percent Rule quickly became a road map to maximizing spending without depleting funds. In other words, it helped retirees go for broke without going broke.

My team tested this rule of thumb in 2014, 2021, and 2023; the numbers still appeared to work. At 4%, the money lasted 40 years, 90% of the time. 84% of the time, it lasted 45 years. Even at the high end of the projection, 50 years, the data show a 74% chance of savings remaining sufficient. A more realistic retirement length of 30 or 35 years edges you and your savings closer to a 100 percent chance of living happily ever after.

As a bonus, Bengen tested the theory at 4.5% and found that by adding small-cap stocks, the money had more than a 90% chance of lasting 30 years.

Using a dynamic approach to your nest egg is frequently the key. Anywhere from 4 percent to 5 percent is repeatedly sustainable if adjustments are made as needed. Sometimes, a more significant withdrawal is okay if the belt is tightened when necessary. Dipping into your nest egg should be flexible, but it needn’t be miserly.

Bottom Line

My 20-plus years of helping people plan for retirement have allowed me to turn my theories into practical analysis. No one can predict the future, but committing to the Five Money Secrets Of The Happiest Retirees can increase the odds and minimize the risks.

It turns out money can help buy happiness, and the price is lower than you might think.

This information is provided to you as a resource for informational purposes only and is not to be viewed as investment advice or recommendations. Investing involves risk, including the possible loss of principal. There is no guarantee offered that investment return, yield, or performance will be achieved. There will be periods of performance fluctuations, including periods of negative returns and periods where dividends will not be paid. Past performance is not indicative of future results when considering any investment vehicle. This information is being presented without consideration of the investment objectives, risk tolerance, or financial circumstances of any specific investor and might not be suitable for all investors. This information is not intended to, and should not, form a primary basis for any investment decision that you may make. Always consult your own legal, tax, or investment advisor before making any investment/tax/estate/financial planning considerations or decisions. Investment decisions should not be made solely based on information contained in this article. The information contained in the article is strictly an opinion and it is not known whether the strategies will be successful. There are many aspects and criteria that must be examined and considered before investing.